How I got cancer. Rami Blekt Intro to number four...

One of the first problems you may encounter in the entrepreneurial field is the lack of real income. The company already exists documented and is a taxpayer, but there is nothing to pay taxes on. You can't let this situation take its course. Tax reporting is an obligation, and for failure to comply with it, you face not only a fine, but also blocking of company accounts.

At the same time, the submission of a zero declaration is enough simple procedure that does not require special experience. You will need a sample zero USN declaration for 2017 (for VAT or UTII on the main taxation system or “imputation”).

You need to take this completed form or send it via the Internet to the tax office. You can download a sample document from the official website of the department. If your state has employees, then the list of documents can be expanded.

In addition to the listed documents, entrepreneurs with employees need to report to off-budget funds: to the Social Insurance Fund and to the Pension Fund.

Legal entities located on (OSNO) pay income tax, and individual entrepreneurs -. In the event that no activity was carried out, the taxpayer submits to the tax office zero declarations for all types of taxes. Reporting is submitted once a quarter. Data for the 1st quarter of 2017 must be submitted by February 29th.

In addition, individual entrepreneurs working for OSNO are required to submit a declaration in the form to the fiscal authority. Change zero reporting on the main system of taxation occurs only through the Internet.

With regard to transport, water, land, corporate property tax, as well as excises, legal entities and individual entrepreneurs are recognized as taxpayers only if they have an object of taxation. If it is missing, then you do not need to submit a declaration.

Submission of zero reporting on the main taxation system occurs only via the Internet.

Entrepreneurs and legal entities on the simplified tax system fill out sections on the first three sheets of the declaration:

1. In the corresponding columns of the first sheet, enter the TIN and KPP (for individual entrepreneurs only TIN), code tax authority.

F. I. O. IP (if the organization - indicate its name).

In the line "" we indicate the data of Rosstat, and in the line "Reliability ..." we enter information about the director of the enterprise. Important: in the section "Adjustment number" is set to "0". In the column "Tax period" put "34" (which means 1 year). Do not forget to enter the date and put your signature.

2. The second page of the zero declaration includes four lines that are important for us. 001 - prescribe "1" or "2" (depending on the object of taxation); 010 - indicate the classifier (); 020 - indicate the object of taxation "income" - 182 1 05 01011 01 1000 110, the object of taxation "income minus expenses" - 182 1 05 01021 01 1000 110. 080 - the data is correlated with line 020. In all other sections we put dashes.

3. On the last page of the declaration on the simplified tax system, line 201 is filled in, in which the tax rate is entered - 6% or 15% (the% sign is not used). Blank cells are filled with dashes. This completes the completion of the zero declaration on the USN.

4. For individual entrepreneurs and legal entities on OSNO, zero reporting is transmitted via the Internet. In this case, special software with an electronic digital signature is used. Programs are supplied with all necessary instructions.

Entrepreneurs and legal entities on the simplified tax system fill out sections on the first three sheets of the declaration.

Thus, it turns out that filling out and submitting a zero declaration to the tax authorities is not difficult task. But ignoring here shines with an unpleasant penalty. states that it can be up to 30% of the amount of unpaid tax, but not less than 1 thousand rubles. Since the amount of the arrears in this case is zero, then the penalty is the minimum limit. But after all, the lost thousand is not a reason for joy.

Submit a zero declaration on time, especially since the procedure for filling it out will allow you to fill your hand to draw up a document showing profit. The last one will be coming soon!

Unlike sleeping pills, taxes are not addictive. Therefore, you can pay all your life. Mikhail Mamchich, aphorist

Unfortunately, in entrepreneurship, things don't always go the way a businessman plans. There are periods of profit, and sometimes, on the contrary, when there is no income. What should an individual entrepreneur (IE) do when his business is “standing still”, is it necessary to submit reports to the tax authorities if he actually has no activity?

In the absence of activity, an individual entrepreneur, like any business entity, is obliged to provide reporting established by law to the bodies of the Federal Tax Service of the Russian Federation (FTS), the bodies of the Pension Fund of the Russian Federation (PF), etc. Since the main form tax reporting entrepreneur is a declaration, then, accordingly, a declaration with values equal to zero is called “zero IP declaration”, and the entire set of reports is “zero IP reporting” or “zero balance”. The situations of their compilation are characterized not only by the absence of directly entrepreneurial activity, but also by the fact that during the reporting period, the individual entrepreneur does not carry out operations on cash and current accounts, is not accrued and is not paid wage employees, if any. In addition, zero reporting is generated for IP newly registered at the end of the reporting period, which simply did not have time to start running a full-fledged business. We can say that in all these cases there is no tax base itself for calculating the amounts of a particular tax, and, accordingly, the declaration becomes zero.

Regarding the term " zero balance”, It should be noted that it is often used as a designation for a special reporting document “balance sheet”, which is used in the activities of legal entities. But in this article, this concept is equivalent to the concept of "zero reporting", as it applies to individual entrepreneurs.

All accounting documents, which form zero reporting of individual entrepreneurs, are compiled in the same forms as the reports of entrepreneurs conducting full-fledged activities.

It is important to remember that for non-submission of tax reporting or its submission in violation of the deadlines, an individual entrepreneur can be held tax or administratively liable. Therefore, even zero reporting by an individual entrepreneur, for whom no activity was carried out, must be compiled and transferred to the authorized bodies within the time limits established by law.

What reports make up the zero balance of IP? The fact is that the answer to this question depends on the tax regime chosen by the entrepreneur. Usually this - General system taxation (OSNO), a simplified taxation system (STS or simplified taxation) and a single tax on imputed income (UTII or imputation).

Composition of reporting

Zero reporting of IP on OSNO will depend on whether the IP has employees. If they are, then the individual entrepreneur must submit quarterly:

And once a year - the average number.

If an individual entrepreneur does not have employees, then his zero reporting will consist of:

The deadlines for submitting a VAT return are set no later than the 20th day of the first month, next quarter.

Declaration 4-FSS is submitted to the Social Insurance Fund (FSS) every quarter before the 15th day of the next month (for example, for the first quarter until April 15, for the second - until July 15, etc.).

The RSV declaration and personal information are also quarterly reports. They are submitted to the Pension Fund before the 15th day of the second month of the next quarter, for example, the 1st quarter ends in March, and information is provided until May 15th. Since, in fact, the activity of the individual entrepreneur is not carried out, in some regions, employees of the PF allow, instead of the established forms of these reports, to submit a letter in any form confirming the absence of entrepreneurial activity.

Reporting features

Speaking about the zero reporting of individual entrepreneurs, one cannot fail to mention such a type of information provision as a single simplified tax return (UND). Such a declaration can be applied by an individual entrepreneur to the simplified taxation system only in relation to VAT, since the individual entrepreneur does not pay all other taxes that it may include. The individual entrepreneur fills out only the first page of the UND, entering information about himself as an economic entity, OKATO of the corresponding region and selects the reporting period - “quarter”, then fill in the VAT data equal to zero. The entrepreneur does not enter other information into the UNM.

In practice, the UND is not often used by IP, since, in fact, it replaces only a zero VAT return. However, entrepreneurs should be aware of this reporting option.

As for filling out a zero VAT declaration, it is also quite simple for self-registration of IP. Here you need to fill out only pages 1 and 2. Since she submits a VAT return at the place of tax registration of the individual entrepreneur, the code is 400.

Filling in the zero declaration 3NDFL is that sections 1 and 6, as well as sheets A, B, G1 and G1 remain empty. The data of the entrepreneur are indicated on the first two pages, the taxpayer code is defined as 720, the country code is 643 - Russia, the document code - passport - 21, the tax period code is -34. Together with the 3-NDFL form, the 4-NDFL form is submitted, where the individual entrepreneur calculates the amount of the estimated annual income. But 4-personal income tax is submitted only if the income will increase (it cannot decrease with zero activity) by more than 50 percent.

Composition of reporting

When working on USN reporting also depends on the presence or absence of employees. If there are such, then the IP provides every quarter:

In addition, once a year, a declaration on the simplified tax system and information on the average headcount at the beginning of the year must be submitted.

If an individual entrepreneur works on the simplified tax system without employees, then he has the simplest zero reporting. There will be no quarterly reports at all, and once a year the entrepreneur will provide:

It should be noted that although an individual entrepreneur on the simplified tax system does not report to the Pension Fund, he must pay insurance premiums to the Pension Fund and the Federal Compulsory Medical Insurance Fund (FFOMS), which are established by law in a fixed amount. In 2013, they amounted to 32,479.2 rubles in the Pension Fund and 3,185.46 rubles in the FFOMS. In 2014 they will amount to 16239.6 rubles. and 3185.46 rubles. respectively (from indicators for individual entrepreneurs with an income of up to 300 thousand rubles).

Reporting deadlines

A zero tax return for an individual entrepreneur on the simplified tax system is submitted once a year until April 30 of the next reporting year. Advance payments during the year in the absence of activity are not accrued and are not paid.

The terms of other reporting documents are similar to the terms of the corresponding forms with zero activity of the IP on OSNO, so it makes no sense to indicate them here again.

Reporting features

When filling out the zero declaration of the simplified tax system, the entrepreneur is guided by the Order of the Ministry of Finance of the Russian Federation No. 58n dated 06/22/2009. Here it will be necessary to indicate only general information on the title page, select the object of taxation (“income” or “income minus expenses”), and the tax rate. The rest of the rows will be zero. Thus, lines 001, 010 and 020 are filled in the first section, and a dash is put in all other lines. In the second section, there will be dashes in all lines except 201.

When the base “income minus expenses” is applied, then in the zero declaration it is possible to show the expenses incurred and carry them over to the next year.

Please note that if in the reporting period the expenses of the IP exceeded the income, but the activity was carried out, one cannot speak of a zero declaration. In this case, a minimum tax of 1% of the IP income in the reporting period is calculated and paid.

Regarding zero reporting at application of UTII you should know that it simply does not happen. This is due to the fact that the very concept of a single tax implies the conduct of business activities of a certain type. If there is no activity, then an individual entrepreneur with such a tax regime does not exist. In this case, the entrepreneur must be deregistered as a UTII payer. At the same time, he can switch to simplified taxation from the next calendar month.

Considering that UTII is a quarterly tax, there may be cases when there was no activity for one or two months, respectively, for these months the individual entrepreneur will not pay UTII.

Thus, it is clear that there can be no completely zero declaration on UTII. Although if you are deregistered as a payer of this tax for one or two months, then when calculating in the declaration for the entire quarter, you can safely indicate the corresponding values of lines 050, 060 or 070 of section 2 equal to zero. But if at least 1 day of the reporting quarter the activity falling under the imputation was carried out, this declaration will no longer be zero.

Zero reporting methods

All zero reporting documents are provided in the same order as regular ones.

They are prepared in duplicate: one is submitted to the regulatory authority, the second with a note on the date of submission remains with the taxpayer.

There are three transmission methods:

For the convenience of understanding the material of this article, you can make a table:

| Tax regime | With employees | No employees | ||

| Report | Delivery time | Report | Delivery time | |

| BASIC | VAT declaration | VAT declaration | Quarterly until the 20th of the following month | |

| Declaration 4FSS | Quarterly by the 15th of the following month | Declaration 3NDFL | Annually until April 30 of the following year | |

| RSV Declaration | Average headcount | Once a year until January 20 | ||

| Personalized accounting | ||||

| Average headcount | Once a year until January 20 | |||

| USN | USN Declaration | Once a year until April 30 | USN Declaration | Once a year until April 30 |

| Average headcount | Once a year until January 20 | Average headcount | Once a year until January 20 | |

| Declaration 4FSS | Quarterly by the 15th of the following month | Pay fixed insurance premiums in PF and FSS | ||

| RSV Declaration | Quarterly until the 15th day of the second month | |||

| Personalized accounting | ||||

| UTII | Does not exist. An individual entrepreneur must be deregistered as an imputed tax payer. | |||

So, do not forget to submit zero reporting, even if entrepreneurial activity was not carried out in a separate reporting period. It is quite simple to fill out, and its timely submission will save you from unnecessary "headache" associated with proceedings in tax and other authorities.

Is a zero declaration on the simplified tax system for 2017 required for individual entrepreneurs in 2018? Where can I download the form in Excel? What does a sample of filling out a zero declaration for an individual entrepreneur with an “income” object look like? We will answer questions and give examples of filling (they are available for download)

If in 2017 an individual entrepreneur did not conduct business and did not have any operations on accounts, then this does not relieve him of the need to fill out and submit a zero declaration form for the simplified tax system for 2017. Having downloaded such a declaration, the tax authorities will simply understand that there were no incomes in 2017. That is, the IP, one might say, declares zero activity in 2017.

By general rule, the deadline for filing an IP declaration of the simplified tax system for 2017 is no later than April 30 of the year that follows the past tax period. That is, formally, you need to be in time before April 30, 2018 inclusive. It will be Monday, however, an official non-working day.

For tax return IP on USN terms change almost always falls along with the first May holidays. The situation is the same in 2018. Therefore, the deadline for submitting the tax return of the simplified tax system for individual entrepreneurs for 2017 is due to clause 7 of Art. 6.1 of the Tax Code of the Russian Federation moves to May 03 - Thursday. This will be the first working day after the extended May holiday. For details, see "". No later than this, for individual entrepreneurs, a zero declaration form for 2017 must be submitted to the Federal Tax Service Inspectorate.

CONCLUSION

Even if an entrepreneur on the simplified tax system with the object of taxation "income" did not receive any income in 2017, then he must submit a zero declaration on the simplified tax system to his IFTS no later than May 3, 2018.

For submitting a zero declaration on the simplified tax system for 2017 in violation of the deadline, a fine of 1,000 rubles is threatened. (Clause 1, Article 119 of the Tax Code of the Russian Federation). But you can try to reduce the amount of the fine if there are extenuating circumstances, for example, if there is a slight delay in submission (clause 1, article 12 of the Tax Code of the Russian Federation, clause 18 of the Decree of the Plenum of the Supreme Arbitration Court of the Russian Federation dated July 30, 2013 No. 57). To do this, along with the declaration on the simplified tax system, submit a letter to the IFTS with a request to reduce the amount of the fine and indicate extenuating circumstances.

For violation of the deadlines for filing tax returns, not only tax, but also administrative liability is provided. According to the statement tax office may issue a warning or fine the head or chief accountant of the organization in the amount of 300 to 500 rubles. for each untimely submitted declaration (Article 15.5, paragraph 4, part 3, Article 23.1 of the Code of Administrative Offenses).

For a delay in filing a declaration under the simplified tax system, the inspectorate has the right to block the bank accounts of an organization or individual entrepreneur on the simplified tax system. The account may be blocked if the organization has not submitted a declaration within 10 working days after the deadline for its submission has expired (clause 3, article 76, clause 6, article 6.1 of the Tax Code). For individual entrepreneurs, the rules on blocking accounts apply in full for failure to submit a declaration on the simplified tax system for 2017.

Fill out the title page with all the required information. When submitting a paper declaration, in the remaining sections of the Declaration, indicate the TIN, KPP and page numbers.

And in all other cells of the lines, put dashes (clause 2.4 of Section II of the Procedure for filling out the declaration), except for:

The composition of the zero declaration on the simplified tax system for individual entrepreneurs looks like this.

All payers of the simplified tax at the end of the year must submit a declaration on the simplified tax system to the tax office at the place of registration, depending on the chosen object of taxation. Lack of activity and (or) income does not affect the obligation of the simplifier to submit annual reports to the tax authorities. If an individual entrepreneur or organization did not conduct activities during the year and (or) did not receive taxable income, they must submit a “zero declaration” to the IFTS at the place of registration.

Note: if the simplified person does not conduct activities and no transactions go through on the current account, he can submit a single simplified declaration, consisting of only one sheet.

The “zero” declaration of the simplified taxpayer using the “income” object consists of following sheets:

Individual entrepreneurs or organizations using “income reduced by the amount of expenses” with the object submit reports consisting of:

As well as the usual declaration on the simplified tax system (with income indicators), the zero one is submitted in the following terms:

You can submit zero reporting to the tax authority:

Step-by-step instructions for filling out the zero declaration of the USN

Note: since in the "zero" reporting information is entered only in Title page, and zeros are put in the rest, then we will not dwell on filling out sections 1.1, 1.2, 2.2 and 2.1.1 and will only give screenshots of these pages.

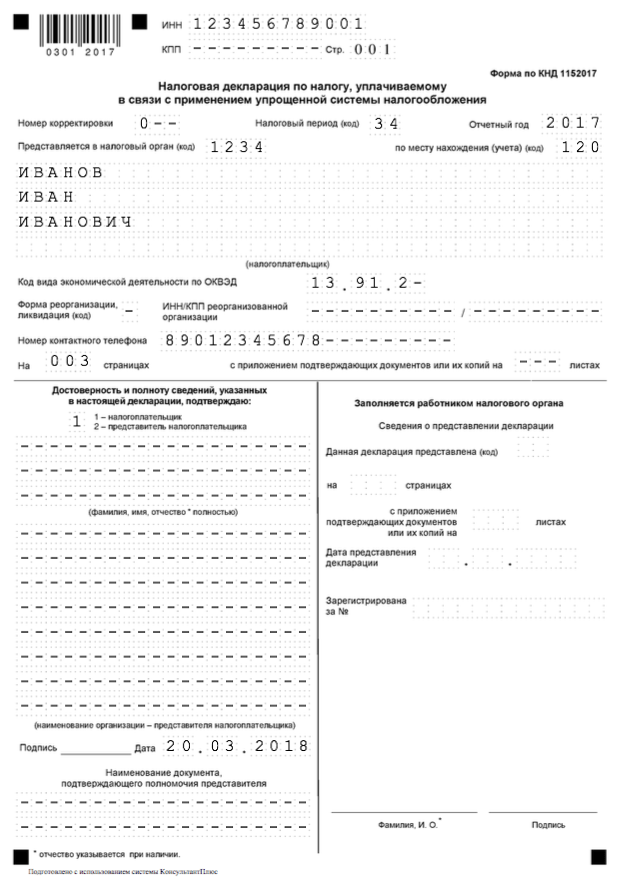

Title page of the zero declaration on the simplified tax system for individual entrepreneurs and LLC

Column/row Note TIN/KPP Organizations indicate TIN and KPP, IP only TIN Correction number If the declaration is submitted for the first time (primary), then the adjustment number will be «0-». If the second and subsequent times (in order to correct an error in previously submitted statements), then the number "2-", "3–" etc. depending on which account the amended declaration is submitted

Taxable period "34"- if the reporting is submitted for the year "fifty"- when submitting a declaration after the liquidation of the organization or the closure of the IP

"95"- when switching to another taxation regime

"96"- upon termination of activities under the simplified tax system

Reporting year Year for which the declaration is submitted Submitted to the tax authority The four-digit code of the tax authority in which the LLC or individual entrepreneur is registered By location (code) Organizations when filling out choose one of two codes: "210"- at the location of the LLC

"215"- at the location of the assignee

IP indicate only one code - "120"

Taxpayer Organizations indicate the full company name in capital letters. Please note that there must be one empty cell between LLC (in decoded form) and the name itself, even if the name falls on the next line.

An individual entrepreneur in this field reflects his full name, without indicating his status (“individual entrepreneur”)

OKVED code Main activity code, in accordance with OK 029-2014 (NACE Rev. 2) Contact phone number The current phone number by which the checking inspector can contact the taxpayer and clarify his questions. The phone number is in the format + 7 (…)…….

On … pages Zero declaration will always have only 3 sheets, which must be specified in the following format: "003" I confirm the accuracy and completeness of the information .... If a company submits reports, it indicates: "one"- if the declaration is filled in and submitted by the director of the LLC, his full name is indicated in the lines below.

"2"- if the declaration is submitted by a representative, the full name of the representative and the name of the document confirming his authority are indicated below

If an individual entrepreneur submits reports, he also chooses one of two codes:

"one"- if he independently fills out and submits reports, while dashes are placed in the lines below.

"2"- if the declaration is filled in and submitted by his representative, while the lines below indicate his data and information about the document on the basis of which he acts

the date Date of completion of the document Section 1.1

By order of the Federal Tax Service of Russia in mid-2014, it was approved new form tax return under the simplified tax system (order No. ММВ-7-3/352). It is in this form that you need to report on the results of 2015. The reporting deadline for organizations using simplified taxation is the last day of the first quarter of 2016, and for individual entrepreneurs - the first working day of May 2016, since April 30 falls on a day off.

The declaration is submitted in any of three ways, namely:

For some organizations, there is a direct obligation to submit a tax return via the Internet, but This obligation does not apply to simplists., since the number of employees in these companies cannot exceed 100 people.

The new declaration has special sections that need to be filled out depending on the object of taxation. There is also a section for organizations that receive funds in the form of targeted funding or charitable contributions. It is only necessary to submit completed sheets to the tax office, that is, if you did not fill out some section, then you do not need to submit it to the inspectors. In the order of filling, by the way, this is clearly stated only for the third section of the declaration.

Individual entrepreneurs who apply the simplified tax system and have received an indulgence from the regional authorities in the form of tax holidays often think that since they do not pay tax, they should not submit reports. This is not true! Everyone must report and tax holidays do not at all exempt from paying tax, but only allow it to be applied at a rate of 0 percent. Below we provide instructions for filling out a “simplified” tax return, and at the end of the article there will be a link to the form (declaration form), and you can also download a completed sample for free.

General rules for filling out the declaration

On each sheet of the declaration for the simplified tax system for 2015, it is necessary to indicate the TIN of the taxpayer. Legal entities must also register their checkpoint. Both can be taken from the notice of taxpayer registration received from the tax office.

1. In the "Adjustment number" field, enter the value "0—".

2. In the "Tax period" field - the code of the tax period for which you submit reports. So, if the declaration is submitted at the end of the year, then the value of the code will be "34", but if you fill out the reporting during the reorganization of the enterprise - "50". Order No. MMV-7-3 / 352 will help to accurately determine the code in a given situation.

3. In the "Reporting year" field, the year for which the reporting is submitted is indicated.

4. In the field "Taxpayer" entity must indicate its full name. It must match the name specified in the founding documents. IP in this field puts down his last name, first name and patronymic. There should not be any abbreviations, the information must correspond to passport data.

5. In the field "Type code economic activity according to the OKVED classifier "you need to enter the appropriate code. It is registered in the extract from the Unified State Register of Legal Entities (for individual entrepreneurs - from the Unified State Register of Legal Entities). You can get an extract from your tax office or on the website of the tax service. You can also find out the code itself from the classifier. If an organization applies several tax regimes at once, then the code must be indicated only for those types of activities for which a simplified tax is paid.

Rules for filling out sections 2.1 and 2.2

Sections 2.1 and 2.2 are filled in depending on the chosen object of taxation. Accordingly, it is most convenient to fill them in the first place.

It is filled out by organizations and individual entrepreneurs who pay tax only on income. In this section, you must specify all payments or income that are not deductible for tax purposes. Consider the order of filling in the individual lines of the section:

1. Line 102

If the organization or individual entrepreneur has payments to employees, the number 1 is put in this line, if the individual entrepreneur does not have such payments, the number 2 is put.

2. Lines 110-113

Designed to indicate the total amount of income for the reporting periods. Recall that such periods for simplistic people are quarters and a year. The amounts are calculated on an accrual basis.

3. Lines 130-133

Here, as a cumulative total, you must indicate the amount of advances for each reporting period, as well as the total amount of tax calculated for the year. Insurance premiums should not be taken into account.

4. Lines 104-143

These lines indicate the amounts of contributions for compulsory insurance, as well as the amounts of payments for temporary disability leaves for which you have reduced tax.

This section is filled out only by those taxpayers who calculate tax on income reduced by expenses.

Consider the order of filling in the individual lines of the section:

1. Lines 210-213

This includes the amount of income for the reporting periods. As always, the cumulative result.

2. Lines 220-223

By the same principle, here you need to specify the amount of expenses.

3. Line 230

Here the amount of the incurred loss (or part of it) for the previous tax periods is fixed.

4. Lines 240-243

Designed to enter the tax base for each period. You can calculate it by calculating the difference between income and expenses. Do not forget to take into account the amount indicated in line 230. It is deducted from total amount per year.

5. Lines 250-253

Filled in if the calculation of the difference between income and expenses turned out to be a negative number.

6. Lines 260-263

Here are the tax rates applicable in each particular period. In general, the rate is 115 percent, but it may be reduced by regional regulations.

7. Lines 270-273

Needed to reflect advance payments. They will be equal to the product of the numbers indicated in lines 240-243 and the rates indicated in lines 260-263.

8. Line 280

The minimum amount of tax should be indicated here. For the simplified tax system, it is calculated by multiplying the income received by 1 percent. If your calculations show that the tax payable is less than this amount, you will have to pay the minimum tax.

Rules for filling out section 3

If your organization did not receive earmarked funding during the reporting period, you can safely skip this section. If you were transferred any targeted funds, then you will have to fill it out. Incidentally, this funding does not include subsidies provided to autonomous institutions. For exact definition types of financing, you can refer to the Tax Code (Article 251).

In this section, you must indicate the amounts of subsidies that were not used in the previous year and for which the period of use has not yet expired.

In section 3, respectively, the following information is also indicated in the columns:

1. Code of the type of transferred funds. You can determine it in accordance with Appendix 5 to the procedure for filling out reports.

2. Date of receipt of property or funds.

3. The amount of funds received, the period of use of which has not yet ended, and also which do not have a period of use.

The remaining columns provide information on the amounts that were transferred to the organization in the reporting year. Thus, the second and fifth columns are filled in by those who received funding with a specified period of use, and the seventh column indicates funds that were not spent in accordance with the intended purposes. Property is stated at market value.

Rules for filling out sections 1.1 and 1.2

These sections are very easy to fill in according to the indicators already indicated in section 2.1 or 2.2. Here you need to reflect the amount of the calculated amount of advance payments and tax. Similarly to sections 2.1 and 2.2, sections 1.1 and 1.2 are filled in depending on the object of taxation.

1. Lines 010, 030, 060, 090

Here you need to register the OKTMO code. If for the entire tax period the location of the organization or the place of residence of the individual entrepreneur has not changed, then only 010 is filled in.

2. Line 020

This includes the amount of the advance payment for the first quarter.

3. Line 040

The amount of the advance payment for the six months, reduced by the number indicated in line 020, is indicated. If, as a result of subtraction, you get a number with a minus sign, then this difference must be indicated in line 050.

4. Line 070

Here, similarly to the previous situation, an advance payment for 9 months is indicated.

5. Line 080

To be filled in if the difference is negative and the advance payment needs to be reduced.

Lines 100 and 110 are filled in the same way.

Section 1.2 is filled in by those organizations and entrepreneurs who have chosen income reduced by the amount of expenses as an object of taxation.

The rules for filling out section 1.2 correspond to the rules for section 1.1 above. The only difference is line 120, in which you need to calculate the minimum amount of tax for the year.

On our website using an online calculator.

How I got cancer. Rami Blekt Intro to number four...

Luck is one of the most unpredictable phenomena in a person's life. Its impossible...

The other world is a very interesting topic that everyone thinks about at least ...