(1908-1954) - Soviet statesman and military figure, Colonel General,...

FGOU VPO Financial Academy under the Government of the Russian Federation (FINACADEMY)

Department "Evaluation and management of property"

Abstract on the topic:

"Economic value added

( EVA )»

Performed : student of FM group 4-2

Kalabashkina E.

Scientific adviser: Tulina Yu.S.

Moscow

In the 1970s - 1980s in companies developed countries the question arose of developing a new mechanism financial management. This was explained by the fact that the methods of evaluating the company's activities that existed until that time could no longer meet the growing requirements of managers, since they did not allow evaluating the company's activities in the long term. In addition, investors began to demand from the management of companies a constant increase in the value of the company - an indicator that reflects the level of wealth of shareholders.

The concept of economic value added (EVA™), developed in the USA in the 80s of the last century, solved the problems posed. Based on the principle of economic profit, the EVA indicator could be used to determine the value, as well as to characterize the long-term performance of the company.

This concept quickly began to be applied by the leading American companies, such as Coca-Cola, General Electric. Soon their experience began to be adopted by firms (including small ones) in other countries.

Russia currently has the opportunity to borrow the most advanced foreign technologies and business methods, which always gives the “catching up” country an advantage over the “overtaking” one. In this regard, it is important for domestic companies to immediately implement and use advanced management mechanisms. The use of the concept of economic value added, which is one of the advanced concepts of financial management, will allow domestic firms to improve performance and reduce the gap from foreign competitors.

Despite positive experiences abroad, the concept of economic value added is currently little applied. Russian companies. The main reason for this is the complexity of its application "in its pure form" in the Russian economy. Accordingly, determining the possibility and developing mechanisms for using the concept of economic value added in the financial management of Russian companies is an urgent task of financial science.

The object of this study acts as the process of financial management of the company.

Subject of study- mechanisms of financial management of the company, based on the concept of economic value added.

Theoretical and methodological basis of the study made up the works, first of all, of foreign experts in the field of corporate finance, valuation, company cost management and, in fact, the concept of EVA.

Among the classic works of the theory of finance, the works of F. Modigliani, M. Miller, E. Pham and W. Sharp, S. Ross, S. Pratt should be singled out.

Of the works devoted to the concept of EVA, first of all, it should be noted the work of its author B. Stewart "The Quest For Value: a Guide for Senior Managers", as well as the book by D. Young and S. O'Byrne "EVA and Value-Based Management: a Practical Guide to Implementation. Among the empirical works that examine the results of the implementation of EVA in practice, it is worth highlighting the works of S. Weaver, G. Biddle and R. Bowen.

In the 70-90s, two concepts for assessing the cost and efficiency of enterprises appeared, among which the most popular in last years are balanced scorecard(BSC) and economic value added(EVA).

Development of the paradigm for determining the value and efficiency of the firm

| 1920s | 1970s | 1980s | 1990s |

The DuPont Model; · Return on investment (ROI) |

· Net earnings per share (EPS); Share price to net profit ratio (P/E) |

· Coefficient of ratio of market and book value of shares (M/B); · Return on equity (ROE); · Return on net assets (RONA); · Cash flow(Cash flow) |

· Economic value added (EVA); · Earnings before interest, taxes and dividends (EBITDA); · Market value added (MVA); · Balanced scorecard (BalancedScorecard -BSC); · Total shareholder return (TSR); Cash flow return on invested capital (CFROI) |

In the Russian-language economic literature, the concept of EVA is considered only in separate works, almost exclusively in translations. EVA is important financial indicator- relatively recently (in the early 90s of the last century) it began to be actively used by many corporations in the USA and some other countries (for example, let's call AT&T, QuarkerOats, Briggs & Stratton, Coca-Cola).

Economic value added ( EVA) represents the profit of the enterprise from ordinary activities, after taxes, reduced by the amount of payment for all capital invested in the enterprise.

The indicator is used to assess the efficiency of the enterprise from the perspective of its owners, who believe that the activity of the enterprise has a positive result for them if the enterprise managed to earn more than the profitability of alternative investments. This explains the fact that when calculating EVA, not only the payment for the use of borrowed funds, but also the equity capital is deducted from the amount of profit. It can be argued that this approach is more economic than accounting.

The author of the concept of "economic added value" D.B. Stewart defined this ratio as the difference between net operating income and capital costs, i.e. E VA allows to estimate the real economic profit at the required minimum rate of return.

Economic value added is an indicator of the company's annual profitability, which primarily shows shareholders whether the company has managed to create additional value. EVA can also serve as a goal for top management and be used in a motivation system.

Indicator logic EVA is as follows: net operating profit after tax is the income received after deducting expenses and depreciation. Part of this income is used to pay for the cost of using resources (expressed in the cost of equity and borrowed capital), and the other part is the value created, which is measured by E V A. This concept proceeds from the fact that it is not enough for a company to have a positive financial results or an acceptable level of earnings per share, any business unit in the course of its economic life must reach such a level of development that it is possible to create new value. And it is created only when the company receives a return on invested capital that exceeds the cost of raising capital.

Economic value added is calculated by the formula:

| EVA = NOPAT - Capital = NOPAT - WACC * CE |

EVA ( economic value added ) - Economic value added.

NOPAT ( Net Operating Profit After Tax ) - net profit received after paying income tax and minus the amount of interest paid for the use of borrowed capital. That is, this is the net profit according to the data financial reporting(according to the Profit and Loss Statement), taking into account the necessary adjustments.

Capital ( cost Of Capital ) - the total cost of the company's capital (consists of equity and borrowed capital, measured in absolute units).

WACC ( Weight Average cost Of Capital ) - weighted average cost of capital (measured in relative values- in%), this is the cost of total capital (own and borrowed).

CE ( Capital Employed ) - invested capital. Represents capital, determined taking into account the cost of resources not included in the balance sheet. Calculated by adjusting the financial statements.

Cost of invested capital ( CE ) is calculated by the formula:

CE = TA – NP , where

TA ( Total assets ) - total assets (according to the balance sheet),

NP ( Non Percent Liabilities ) - interest-free current liabilities (according to the balance sheet), that is, accounts payable to suppliers, the budget, advances received, other accounts payable.

Weighted average cost of capital ( WACC ) is calculated by the formula:

WACC= Ks *ws+ kd * Wd * (1 - T), where

Ks- price equity (%),

ws- share of own capital (in %) - according to the balance sheet,

kd- cost of borrowed capital (%),

wd- the share of borrowed capital (in %) - according to the balance sheet,

T- income tax rate (in %)

Cost of equity ( Ks ) is calculated by the method CAPM :

Ks = R + b * (Rm - R) + x + y + f, where

R- risk-free rate of return (for example, the rate on deposits) (%),

Rm- average profitability of shares in the stock market (%),

b- coefficient "beta", which measures the level of risks,

x- premium for risks associated with insufficient solvency (%),

y- premium for the risks of a closed company associated with the unavailability of information about financial condition and management decisions (%),

f- country risk premium (%).

The cost of borrowed capital ( kd ) is calculated by the formula:

kd = r * (1 - T ), where

r- annual interest rate for the use of borrowed capital,

T- Income tax rate.

From the formula for economic value added, you can derive a relative indicator "Return on invested capital" ( return on Capital Employed , ROCE ). economic sense this indicator is that economic value added (EVA) arises in the company in the event that over a given period of time it was possible to earn a return on invested capital (ROCE) higher than the investor's rate of return (WACC).

Investors (owners, shareholders) will not consider themselves satisfied if the return on their capital earned in the company has not reached the threshold rate of return set by them.

This principle of company value formation is expressed in terms of economic value added (EVA):

| EVA = Spread * CE = (ROCE - WACC) * CE |

Spread– yield spread (difference) between the return on invested capital and the weighted average cost of capital. The spread represents economic value added in relative terms (in %).

Spread = ROCE – WACC

If the Spread is positive, then the company has earned a return that exceeds the return required by investors. In this case, the return on capital invested in the company is higher than the alternative return for the investor, because all alternatives are evaluated and taken into account in the indicator of the weighted average cost of capital (WACC). Therefore, the end result - the emergence of economic value added means an increase in the cost of capital over a given period.

ROCE (Return on Capital Employed)- Return on invested capital:

ROCE=NOPAT/CE

Essence EVA manifests itself in the fact that this indicator reflects the addition of value to the market value of the enterprise and the assessment of the effectiveness of the enterprise through determining how this enterprise is valued by the market.

Market value of the enterprise = net assets (at book value) + EVA future periods, reduced to the present time

The value of EVA determines the behavior of the owners of the enterprise in relation to investing in this enterprise:

1. EVA = 0 , i.e. WACC= ROI and the market value of the enterprise is equal to the book value of net assets. In this case, the owner's market payoff from investing in this enterprise is zero, so he equally wins by continuing operations in this enterprise or by investing in bank deposits.

2. EVA >0 means an increase in the market value of the enterprise over the book value of net assets, which encourages owners to further invest in the enterprise.

3. EVA <0 leads to a decrease in the market value of the enterprise. In this case, the owners lose the capital invested in the enterprise due to the loss of alternative returns.

From the relationship between the market value of the enterprise and the values of EVA, it follows that the enterprise must plan the future values of EVA to guide the actions of the owners to invest their funds.

The expectation of future EVA values has a significant impact on the growth of the company's share price. If expectations are inconsistent, the share price will fluctuate, and in the short term it will not be possible to draw a clear relationship between the EVA values and the company's share price. Therefore, the task of profit planning, and with it the planning of the structure and price of capital, is a priority for the management of the enterprise.

The concept of EVA is often used by Western companies as a more advanced tool for measuring the performance of departments than net profit. This choice is explained by the fact that EVA evaluates not only the final result, but also the price at which it was received (ie, how much capital and at what price was used).

1. Increasing profits when using the same amount of capital;

2. Reducing the amount of capital used while maintaining profits at the same level;

3. Reducing the cost of raising capital.

Separately, it is possible to single out a reduction in the amount of taxes and other obligatory payments within the framework of tax planning, using various schemes allowed by the legislation of the Russian Federation.

The indicated ways to increase EVA are implemented in specific activities carried out by enterprises. If the EVA indicator is chosen by the enterprise as a criterion for evaluating the effectiveness of its activities, then the task is to increase the value of this criterion. Such an increase occurs both as part of the reorganization of the enterprise, and as part of the current management activities.

Measures aimed at improving the efficiency of the enterprise

|

In general, summing up, we can outline the role played by the indicator of economic value added in assessing the effectiveness of an enterprise:

· EVA acts as a tool that allows you to measure the actual profitability of the enterprise, as well as manage it from the position of its owners;

· EVA is also a tool that shows the leaders of the enterprise. how they can affect profitability;

· EVA reflects an alternative approach to the concept of profitability (transition from the calculation of return on invested capital (ROI), measured in percentage terms, to the calculation of economic value added (EVA), measured in monetary terms);

EVA acts as a tool for motivating enterprise managers;

· EVA improves profitability primarily by improving the use of capital, rather than focusing on reducing the cost of capital.

Thus, it can be assumed that the use of the EVA indicator in management accounting will improve the quality of assessing the effectiveness of Russian enterprises.

The indicator of added economic profit can be increased by:

1. increase return on existing capital, which can be achieved by increasing prices or margins, increasing volumes or reducing costs;

2. growth in profitability, which can be achieved by investing capital in projects with growing profits and an adequate cost of additional capital, while investments in working capital and production capacity may be required to increase sales, promote new products or develop new markets;

3. optimization of investments, which can be achieved by rationalizing, eliminating or reducing investments in operations that cannot provide a return on the cost of capital;

4. optimization of the cost of capital, which can be achieved by reducing the cost of capital, while maintaining the financial flexibility necessary to implement the strategy of using debt, management risk and other financial instruments.

Thus, there are three ways to increase the added economic profit: to increase profit using the same amount of capital; reduce the amount of capital used, while maintaining profit at the same level; and reduce the cost of raising capital.

The concept of company value management based on the economic value added method is proposed to use the economic value added indicator (EVA) as the main criterion for evaluating the company's activities.

The goal of value management is to maximize the value of a company through the continuous growth of economic value added (EVA). And the way to manage the cost is to manage the factors that affect the value of the company.

The performance of a company is influenced by a wide variety of factors. They can be classified as factors of the external and internal environment (that is, macro- and microeconomic factors). The former influence the performance of the company from the outside, the latter from the inside.

Internal factors affecting the cost can be:

Growth rate of sales of the company's products/services

· Growth rates of the main items of the Balance Sheet and Profit and Loss Statement

Net profit growth rate

The rate of return of the owner (shareholder, investor)

Other factors

External factors affecting the cost can be:

Level of investment, marketing, financial, production and organizational risks of the company

Change in the cost of borrowed capital (interest rate on loans)

Change in tax rates

Economic value added is an important economic indicator that characterizes the efficiency of using the capital of an enterprise, adding to the market value of an enterprise. Economic value added is the real economic income calculated on the basis of the difference between the profit earned and the profit required by the owner, determined using the cash basis of income and expenses.

Economic value added, economic profit and other indicators of residual profit have clear advantages over accounting profit as a criterion for evaluating performance.

EVA serves as a constant reminder to managers to invest when and only when the return on investment is sufficient to recoup the cost of capital. For managers accustomed to focusing on accounting profit or earnings growth, this "signal" is relatively easy to pick up. The EVA criterion can be based on incentive and reward systems suitable for all levels of the organization, down to the lowest. For senior management, such systems can replace close monitoring. With EVA-based compensation systems, management no longer has to call on lower managers not to waste capital and then check whether they follow this order. The use of EVA implies the delegation of authority and responsibility.

EVA gives managers a visual representation of the cost of capital. An enterprise manager can improve EVA in two ways:

1) increasing profits;

2) by reducing the involved capital.

Because of this, the manager has an incentive to get rid of underused assets or transfer them to other hands. Working capital may also decrease.

The indicator of economic value added has a number of disadvantages: this indicator does not reflect the forecast of future cash flows and, therefore, the present value. On the contrary, EVA is determined only by the profit of the current year. Accordingly, it encourages managers to pursue projects with a quick payback and discourages projects that start to pay off later. Similar problems are associated with the launch of a new venture, when huge capital investments are required, and the profit in the early years is low or even negative. And this is not equivalent to a negative net present value, since later profit and cash flow will increase significantly. But initially, the economic value added will be negative, even if the project is projected to have a high positive net present value across all parameters.

Among the shortcomings of the concept are the following:

EVA does not take into account differences in the size of the companies under study;

EVA calculation is based on accounting indicators;

· The EVA indicator does not reflect the causes of possible problems in the company's activities.

The ability to calculate EVA not only when evaluating an investment project, but also as an indicator of the company's performance for any period is its significant advantage in comparison with traditional indicators, such as income or profitability. This advantage is due to the fact that the EVA concept is based on an integrated approach to three main areas of management:

preparation of the capital budget;

Evaluation of the performance of departments or the company as a whole;

· development of an optimal fair system of bonuses for management.

The benefits of applying the concept in the first two areas are associated with an adequate and easy determination of the degree to which a division, firm or individual project has achieved the goal of increasing market value.

Unfortunately, most companies use traditional indicators of performance assessment, namely: profit and marginal profit, sales volumes, income, etc., which can show a distorted picture of the state of the company from the standpoint of its "health" in the long run.

Regardless of the size of the company, the continued creation of value for investors is the main goal of all commercial organizations, therefore, an objective assessment of the effectiveness of invested funds is no less important.

Today, EVA is the most accurate way to assess the effectiveness of a company. It is even more accurate than traditional returns because it includes the present value of capital.

In most cases, the use of EVA is the first step towards the implementation of a system of continuous improvements and the subsequent application of modern management tools.

1. Osipov M.A. Using the concept of economic value added to improve efficiency and measure the company's activities // History of Management Thought and Business. VI international conference "Problems of measurements in organization management". Moscow, June 23-25, 2007 / Ed. IN AND. Marsheva, I.P. Ponomarev. - M.: MAKS Press, 2007. - S. 98-103.

2. Osipov M.A. Modern mechanisms of enterprise management and measurement of its activities // Finance: Collection of articles. - M .: Company Sputnik +, 2008. - P. 95-126.

3. http://www.cfin.ru/management/controlling/evalution.shtmlEVAlution of the balanced scorecard Konstantin Redchenko, Ph.D., Associate Professor of the Lviv Commercial Academy

4. http://1fin.ru/?id=185

L.I. Schneider Kuban State University

5. Damodaran A. Investment evaluation. Tools and techniques for assessing any assets / A. Damodaran: Per. from English. Moscow: Alpina Business Books, 2005.

6. Teplova T.V. Investment leverage to maximize the value of the company. The practice of Russian enterprises. M: Vershina, 2007.

7. Copeland T., Murrin J. Company value: evaluation and management. M.: Olymp-Business. 1999.

8. D. Young, S. O'Byrne. EVA and Value Based Management. A Practical Guide to Implementation - McGraw-Hill - 2000, Chapter 1, 2, 6, 9

EVA™ is a registered trademark of the consulting company SternStewart & Co. Next is EVA.

Stewart B. The Quest For Value: a Guide for Senior Managers. - New York: HarperCollins Publishers, 1991.

http://www.cfin.ru/management/controlling/evalution.shtml

EVAlution of the balanced scorecard Konstantin Redchenko, PhD in Economics, Associate Professor of the Lviv Commercial Academy

http://www.finanalis.ru/litra/324/2293.html Economic value added Elena Larionova Consultant for financial analysis and planning, CG "Voronov and Maksimov", lecturer at the Faculty of Economics, St. Petersburg State University http :// www . vmgroup . en /

Http://1fin.ru/?id=185L.I. Schneider Kuban State University

Gross value added (GVA) characterizes the final result of production activity and represents the value added by processing in this production process. At the level of sectors of the economy, GVA is determined by subtracting intermediate consumption (IC) from gross output (IG). At the same time, the GVA includes the cost of fixed capital consumed in the production process (depreciation).

Intermediate consumption - it is the cost of products and services that are consumed during the current period in order to produce other goods and services: material resources; office and household expenses; payment for transport, communication, VC services; travel expenses; current repair of buildings; advanced training of employees, etc. Depreciation is not included in intermediate consumption.

The absolute increase in GVA in total is calculated as follows:

including:

a) due to changes in labor costs

b) due to changes in labor productivity

c) due to a change in the share of gross value added in gross output (or a change in the share of PP in BB)

where  - index of time spent;

- index of time spent;

- labor productivity index;

- labor productivity index;

- the share of GVA in the gross domestic product of the reporting and base periods, respectively (this may also be the share of intermediate consumption in gross output),

- the share of GVA in the gross domestic product of the reporting and base periods, respectively (this may also be the share of intermediate consumption in gross output),

,

,

- GVA of the reporting and base periods, respectively,

- GVA of the reporting and base periods, respectively,

- gross output of the reporting period.

- gross output of the reporting period.

Gross domestic product(GDP) is the result of production activities in the economic territory of a given country, i.e. it is the result of the activities of both residents and non-residents. It is the value of goods and services produced and therefore does not include intermediate goods and services.

Gross national product- it is the result of the activities of residents of the country, regardless of whether it is produced in the economic territory of this country or outside it.

GDP can be calculated by three methods: production, distribution and final use.

GDP calculated production method, reflects the contribution of each sector of the economy and their individual subjects to the creation of a single macroeconomic result. Thus, in this case, analyzing GDP, one can follow its production structure, as well as the tax structure of the economy.

The calculation of GDP by the production method involves the summation of the gross value added created in all sectors of the economy (  ), and net taxes (N-S), i.e. the difference between the amounts of taxes and subsidies on products and services, including imported ones.

), and net taxes (N-S), i.e. the difference between the amounts of taxes and subsidies on products and services, including imported ones.

In corporate finance economic value added(EVA, developed and registered trademark of the consulting company Stern Stewart & Co) is considered as an indicator of intra-company efficiency and serves as a measure of the value created by a company in a single period of time (month, quarter or year). Economic value added is a financial measure of what economists sometimes refer to as economic profit or economic rent.

Economic Value Added (EVA) is a measure of the economic, and not accounting, profit of the company after paying all taxes and reduced by the amount of payment for all capital invested in the enterprise.

Algorithm for calculating the indicator of economic value added: from net operating profit () the payment for the use of equity and borrowed capital is deducted, the remaining amount is the created value, which is measured by EVA.

The logic of the economic value added indicator is that it is not enough for an enterprise to simply have a positive or return per share, it is necessary to ensure a level of profitability that allows not only to receive a return on invested capital that exceeds the cost of raising capital, but also to create additional value .

In the theory and practice of calculating EVA, there are several ways to calculate indicator of economic value added:

EVA = (r-c) * K = NOPAT - c*K

Where,

r - return on invested capital (), r = NOPAT/K;

c - ;

K - own working capital (capital employed) = total assets - current liabilities.EVA = NOPLAT - DCC = NOPLAT - IC*WACC

Where,

NOPLAT - ;

DCC - normal cost of capital;

IC - the amount of invested capital, calculated by the formula:

IC \u003d (O TA - B TO) + OS + (A P - BO P)

where,

О ТА - operating current assets;

B TO - interest-free current liabilities;

OS - net fixed assets (i.e. real estate, industrial premises, equipment);

A P - other assets;

BO P - other interest-free obligations.

In corporate reports, a modified EVA calculation method is more common, which involves the use of an indicator of return on invested capital - ROCE, i.e. EVA occurs when a corporation or other business entity manages to create a return on invested capital higher than WACC over a certain period of time. Thus, the owners will be satisfied if the return on capital invested in the corporation reaches the established rate of return:

EVA = (ROCE - WACC) * IC = Spread * IC

Where,

Spread - the difference between the return on invested capital and the weighted average cost of capital (yield spread). Spread represents economic value added in relative terms, %.

If Spread > 0, then the corporation received a return in the reporting year that exceeds the return level set by investors.

The use of this option is due to its several advantages. From the calculation, it becomes possible to see the rate of return on capital employed, as well as the size of the gap (Spread) between it and the cost of capital. The percentage value of such a gap is EVA, only in relative terms. The main advantage of EVA compared to all indicators is that, unlike them, it can show the net contribution of the company and its structural divisions to the increase in market value. The high significance of this category is reinforced by the formation around it of a whole scientific approach, called value based management. According to this approach, all company management should be aimed at maximizing EVA, since it is the only criterion for increasing the company's market value.

However, all approaches to calculating the EVA indicator are based on the calculation formula proposed by B. Stewart:

EVA=NOPAT-WACC*IC

Where,

IC (Invested Capital) - invested capital (adjusted amount of total balance sheet assets at the beginning of the reporting period).

For the accuracy of calculating EVA, it was proposed to use 164 adjustments of various indicators, the list of which is closed. At the same time, as B. Stewart noted, in order to use the EVA indicator for management purposes, it is enough to apply only some adjustments that have a significant impact on reporting.

Capital invested (IC), unadjusted, is the difference between total assets and interest-free short-term liabilities:

Where,

IC - invested capital (without adjustments);

NBV (Net Book Value) - total capital (advanced capital);

NPL (Non Percent Liabilities) - interest-free short-term obligations, i.e. accounts payable to suppliers, budget, advances received, other accounts payable.

Economic value added model(economic profit) is one of the models used to estimate the value of a company. In this regard, it is considered that the value of the company is the best tool measure the results of its operations, because its evaluation, as a rule, requires complete information. It is not short-term, unlike other indicators.

The economic value added model assumes that it is on the basis of such an indicator as economic value added that the company's standards should be developed to set goals and evaluate its successes and failures.

The economic value added indicator (EVA) can be considered as a modified approach that combines the requirements and interest of both shareholders and managers of the company to assess its performance.

Using EVA as a tool for assessing the effectiveness of the use of invested capital allows company managers to make more informed decisions on expanding profitable lines of business and, just as important, helps to identify inefficient use of funds in projects whose profitability does not cover the cost of raising capital.

The popularity of EVA leads to the emergence of completely different interpretations of it, different from the originally developed definition. Thus, The Coca-Cola Company understands the difference between the EVA of the reporting and base periods as value added.

The negative point of EVA is the multiplicity of methods for calculating the component of this indicator - the total capital employed, which ultimately can lead to inadequacy when conducting a comparative analysis of two companies based on the EVA indicator.

Despite its shortcomings, the indicator of economic value added is the most effective tool for determining the return on investment in the capital of a company. The quality of disclosure of information about the value added management system directly affects the increase in the investment attractiveness of the company. In the works of modern researchers such as M.A. Vakhrushina, A. Gershun and M. Gorsky, A.I. Krivtsov, D. Martin, V. Petty, contains variants of such reports. Some of the disadvantages of the proposed options for disclosing information about EVA may be that all of the listed authors propose to show investors the final EVA indicator and do not disclose either the sources of its formation or the target orientation for the company's stakeholders. Additional detailing of this indicator can give more full information about the sources of formation of the value of the company, the distribution of these sources, moreover, it will be able to solve the problem of determining the dependence of the volume of capital investments and the share of profit attributed to them.

Company value management is one of the most productive modern concepts management. Leading global companies successfully manage business value in accordance with the system value-oriented management (Value Based Management, VBM) aimed at creating, increasing value based on its assessment and monitoring. VBM is most successfully implemented in public open companies, where the growth of the share price reflects the positive reaction of the market to the results of business development. It is more difficult to manage the value of closed companies.

Increasing the value of a business is in the long-term interests of its owners and other stakeholders. Owners of companies that manage their value increase their wealth while contributing to the wealth of the company's counterparties. Interaction with successfully developing companies is beneficial for both consumers and employees, and the state, and creditors - in a developed market, the capital of inefficiently operating companies will eventually pass to their more successful competitors.

In the process of company value management, the main acceptance criterion management decisions is an indicator of value. The value of the value is estimated using various value added models. The content of value added is defined in the concept of residual income, based on the notion of "residual income", or value added, defined as the difference between a company's profit and the cost of raising capital . The main types of value in the concept of cost management are called added value and will be discussed below.

In the process of company cost management, the following main cost indicators are applicable:

2. Economic value added EVA: calculation formulas

Economic value added (EVA) is the simplest and most common indicator in the value management system, developed by B. Stewart and registered by Stern Stewart & Co.

In the basic case, economic value added can be calculated using one of the following interrelated formulas (1) and (2):

EVA t = EBIT t – WACC × IC (t-1) (1)

The main parameters of formula (1) are involved in the calculation of the return on invested capital ROI= EBIT / IC. Therefore, EBIT = ROI×IC. Then EVA = ROI×IC – WACC×IC = (ROI – WACC) × IC. Thus, the second formula for calculating EVA is:

EVA t = (ROI t - WACC) × IC (t-1) (2)

The main factors of growth in the value of the company according to the model of economic value added (EVA):

Benefits of using Economic Value Added (EVA):

The use of the basic model of economic value added (EVA) allows you to evaluate the value of a business from the perspective of the total invested capital (Enterprisevalue, EV) - by summing up:

At the same time, the developer of the concept B. Stuart determines the need to introduce a large number possible amendments and adjustments to net income and the carrying amount of invested capital.

In particular, in the process of managing the value of one's own company, the result of applying this model must be adjusted by subtracting the market value of long-term borrowed capital.

3. Ohlson, Edwards-Bell-Ohlson (EBO) Models: Calculation Formulas

The Olson model is a modification of the basic model of economic value added, generated not by all invested capital (as in the basic model), but by the company's own (share) capital.

The calculation formulas for the Olson model presented in formulas (3) and (4) are similar to the formulas for the basic economic value added model (1) and (2):

The use of the Olson model makes it possible to evaluate the value of a business from the standpoint of equity using formula (6). For comparison, formula (5) is given next to the calculation of the business value from the position of the entire invested capital (Enterprisevalue, EV).

Substitute expression (4) into expression (6) and assume t=0 — i.e. the value of the company is calculated at the zero point in time; then expression (6) will take the form of formula (7):

For purposes practical application the planning horizon is specified and the forecast and post-forecast periods are distinguished. For each year during the forecast period, direct income forecasts are built. At the end of the forecast period, the difference between the market and book values of the company is calculated.

Thus, formula (7) for practical application looks like this:

Formulas (7) and (8) are EBO model (Edwards-Bell-Ohlson model)(Edwards-Bell-Ohlson EBO) or Olson model(James Olson articles 1990-1995)

The bases of fundamental indicators of Western companies contain forecasts of return on equity (ROE) for the next two years; in this regard, some authors in the process of applying the Ohlson model propose to limit it to two years. Then formula (8) will look like this:

Thus, according to the Olson model, to determine the value of the company, it is necessary to predict the difference (ROE - r e). The cost of equity (r e) can be calculated using or .

Use the Olson model to calculate the business value of a company with a net asset value of 100 units at the valuation date. The rate of return on equity is 15%. In the 1st year of the forecast period, it is planned to receive a net profit of 25 units. and direct to the payment of dividends 5 units. In the 2nd year of the forecast period, it is planned to increase the return on equity by 1.15 times compared to the 1st year of the forecast period.

Solution:

The book value of net assets at the end of the first year (SI 1), calculated on the basis of the book value of net assets at the valuation date (SI 0 = 100 units), profit of the 1st year of the forecast period (25 units) and dividends paid in the first year (5 units), amounted to 120 units. = 100+ 25- 5. Return on equity in the 1st year ROE 1 =(25-5)/ 100=0.2; in the 2nd year ROE 2 =0.2*1.15=0.23. Then, according to formula (9), the cost of the company according to the Olson model will be 160 units.

Used sources:

Valdaytsev C.V. Business valuation and enterprise value management: Proc. allowance for universities. — M.: UNITI-DANA, 2001. — 720 p.

Kosorukova I.V., Sekachev S.A., Shuklina M.A. Valuation of securities and business (+ CD-ROM): tutorial. University Series. - M.: Moscow Financial and Industrial Academy, 2011. - 672 p.

Business valuation: textbook / Ed. A.G. Gryaznova, M.A. Fedotova. - 2nd ed., revised. and additional - M.: Finance and statistics, 2009. - 736 p.

Let's talk about this important criterion assessment of the value of the enterprise as - economic value added ( Economic Value Added). Consider the formula for calculating this indicator, methods for its analysis and management. We will conduct a comparative analysis with other approaches to assessing the company.

In the modern economic environment, economic value added is an indicator of the assessment of the value of a company/enterprise for owners/shareholders.

Economic value added (EnglishEVA,economicvalueadded) - an indicator of the economic profit of the enterprise after payment of all taxes and fees for all capital invested in the enterprise.

Economic value added measures the excess of net operating income after taxes and the cost of capital. The formula for calculating EVA is shown below:

NOPAT(English Net Operating Profit Adjusted Taxes) is operating profit after taxes but before interest payments ( NOPAT=EBIT(operating profit)–Taxes (tax payments));

WACC (English Weight Average Cost Of Capital) is the weighted average cost of capital, and represents the cost of equity and borrowed capital, that is, the rate of return that the owner (shareholder) wants to receive on the money invested;

CE (English Capital Employed, Invested Capital, Capital Sum) – investment capital, is the sum of total assets ( Total Assets) based on the beginning of the year less interest-free current liabilities (accounts payable to suppliers, the budget, received advances, other accounts payable). In the balance sheet, investment capital is the sum of the lines “Capital and reserves” (line 1300) and “Long-term liabilities” (line 1400).

To calculate the weighted average cost of capital (WACC), we use the following formula:

![]()

Where: R e ,R d – expected/required return on equity and debt, respectively;

E/V, D/V - the share of own and borrowed capital in the capital of the enterprise;

t is the income tax percentage rate.

Economic value added shows the efficiency of the company's use of its capital, shows the excess of the company's profitability over the weighted average cost of capital. The higher the value of economic value added, the higher the efficiency of capital use of the enterprise. Efficiency is determined by the excess of profitability and the cost of capital (borrowed and equity). Large values EVA testifies to the high rate of additional return on capital. Comparison of EVA of several enterprises allows you to choose the most investment-attractive one.

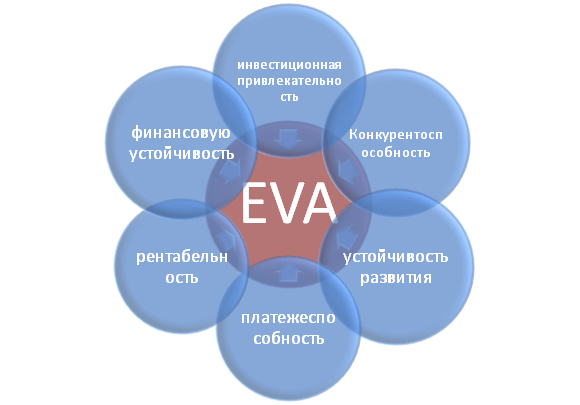

The EVA indicator reflects various categories of an enterprise's activity: investment attractiveness, competitiveness, financial stability, solvency, development sustainability and profitability. The figure shows schematically the relationship between EVA and other enterprise characteristics.

The users of this criterion are shareholders, top managers, investors who evaluate the change in EVA as an integral criterion of economic attractiveness and efficiency of the enterprise development.

| Users | Purposes of use |

| Shareholders/Owners | Estimation of economic added value, analysis of the main factors of its formation, increasing its attractiveness for investors. |

| Top managers | Evaluation of the economic value added of the enterprise and development managerial tasks, regulations, plans and standards to increase this indicator. |

| Strategic investors | Evaluation of the effectiveness of the company's use of its capital, the implementation of mergers and acquisitions of promising companies. |

Based on the EVA indicator, a VBM enterprise management system is built ( valuebasedmanagement). This system enterprise management is based on maximizing the economic value added. The goal of all management decisions at the enterprise is the growth of value for shareholders and owners. Finance serves to create a positive return on investment over invested capital. In this system corporate governance serves to develop a system for measuring the contribution of managers to the growth of the company's value and a system for their material motivation and incentives.

So in her work, Gabriela Chmelíková (in 2008) proved that the EVA indicator has a strong correlation with such classical indicators as ROA and ROE. This proves that EVA is a better indicator of shareholder sentiment than traditional measures. Studies by Klapper, Love, Jang, Kim (2005) have shown that the EVA coefficient has a positive correlation with sales volume, leverage, age and size of the company/enterprise. A particularly strong influence on the EVA indicator is exerted by the corporate one, expressed by the J. Tobin coefficient (Q). These studies once again prove the importance of this indicator, which characterizes the efficiency of the enterprise.

In order to better understand the meaning of economic value added (EVA), let's take a practical example of how this indicator is built. Since all indicators are based on international reporting, they do not exactly match their domestic counterparts. As a result, in a simplified version, the following formula will be obtained:

economicvalueadded= Net income - WACC*(Equity and reserves + Long-term liabilities)

The table below shows the calculation of EVA for OJSC ALROSA.

The net profit of the enterprise is taken from the balance sheet line 2400 and is final result activities of the organization (NOPLAT).

The sum of "capital and reserves" and "long-term liabilities" form the investment capital of the enterprise (CE).

To calculate WACC, you can compare ROE (return on equity, level of profitability) for similar enterprises in the industry. In this example, the profitability of the enterprise's capital management (both own and borrowed) was taken in the amount of 10% per annum.

Economic Value Added = B4-B3*(B5+B6)

Based on the above formula, we can identify the main levers and factors for managing economic value added (NOPLAT, WACC and CE):

Summary

For the sustainable development of a company / enterprise, a single criterion for evaluating the value for owners is needed, which allows you to link the strategic level of management and operational. Economic value added (EVA) is one of the most common indicators for the owner in assessing the value of his business. Based on the EVA indicator, a VBM (Value Based Management) enterprise management model is built, where all enterprise indicators affect changes in value added. To stimulate managers in actions aimed at increasing value, on the basis of this model, various systems evaluation of contributions and monetary incentives.

(1908-1954) - Soviet statesman and military figure, Colonel General,...

General information: Approximate trophy difficulty: 7/10 Offline: 34 (20 , 7 , 6 ,...

Hide and seek is one of the most popular games for children. Kids of all ages love this...